.png)

Insuring the ‘Uninsurable’: Rare Imports & Gray Market Classics in CT

- W. Tom Polowy, MS

- 2 hours ago

- 8 min read

For many automotive enthusiasts in Connecticut, the standard domestic market offerings simply don’t ignite the same passion as the "forbidden fruit" found overseas. Whether it is a right-hand-drive Nissan Skyline GT-R from Japan, a rugged diesel Land Rover Defender from the UK, or a precision-engineered Alpine from France, the allure of the rare import is undeniable. However, the excitement of winning an overseas auction often crashes into a wall of reality when it comes time to secure rare import insurance.

In the world of insurance, "rare" often translates to "risky," and "gray market" can sometimes be interpreted as "uninsurable" by standard carriers. If you have ever tried to add an imported vehicle with an 11-digit VIN to a standard auto policy, you likely encountered a system-generated error and a prompt denial. At Insure Connecticut LLC, we understand that these vehicles are not just "cars", they are historical artifacts and significant investments. We specialize in helping Connecticut residents navigate the complex landscape of insuring vehicles that fall outside the traditional American automotive mold.

The Allure of the Import: Why We Chase the "Forbidden Fruit"

The term "gray market" refers to vehicles that were imported into the United States through channels other than the manufacturer's official distribution network. These cars were never originally intended for the U.S. market, meaning they weren’t built to comply with Federal Motor Vehicle Safety Standards (FMVSS) or EPA emissions requirements at the time of their production.

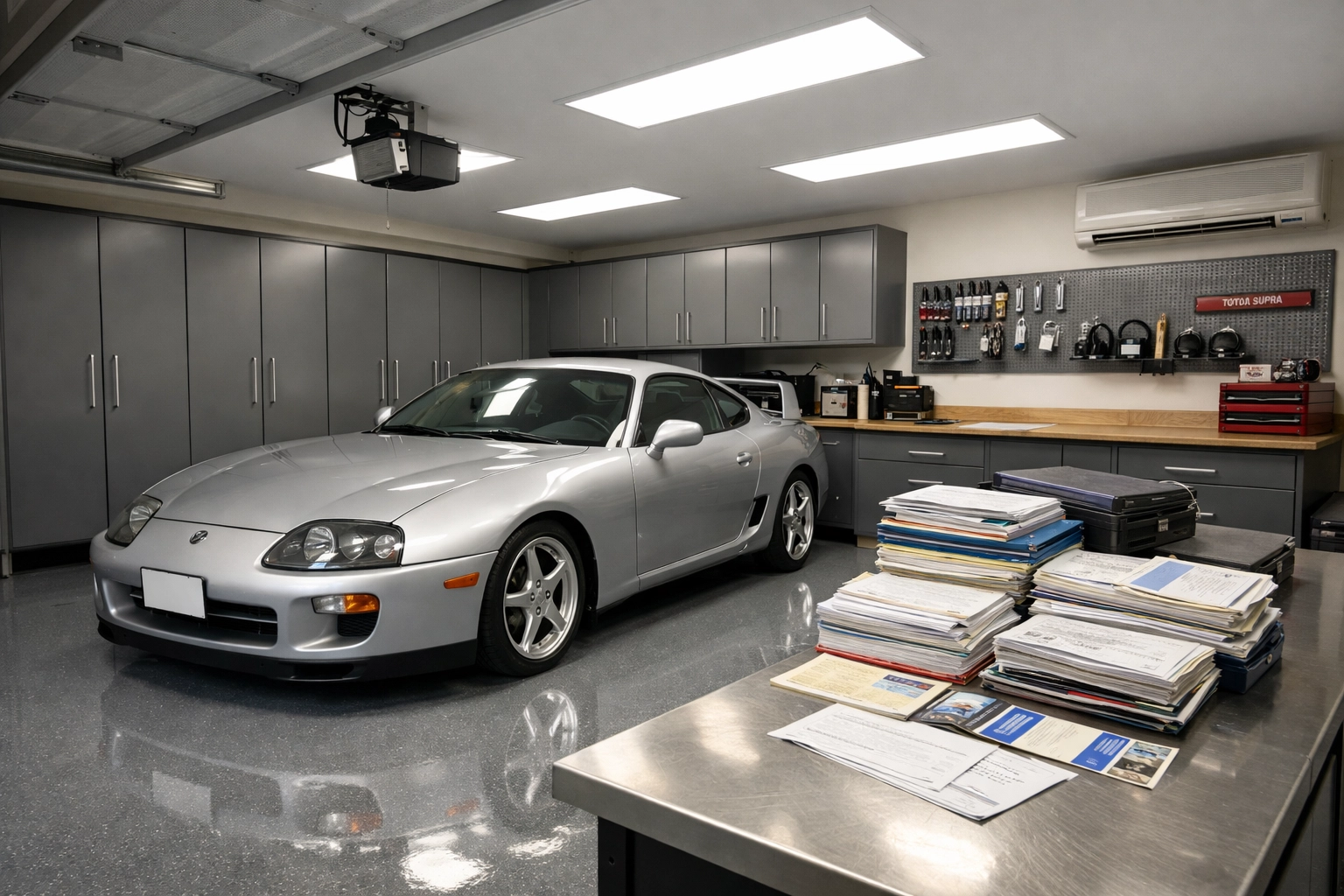

In Connecticut, we see a growing community of collectors who value these vehicles for their unique engineering, cultural significance, and the sheer rarity of seeing one on the Merritt Parkway or parked in downtown West Hartford. The challenge is that most insurance companies rely on automated systems built around standard 17-character Vehicle Identification Numbers (VINs). When you present a 1994 Toyota Supra with a non-standard VIN, most computer systems simply don't know what to do with it. This is where professional brokerage and specialized knowledge become essential.

Understanding the Legal Landscape: The 25-Year Rule

Before discussing insurance specifically, you must understand the legal foundation that makes these cars eligible for the road. The "25-year rule" is the most critical piece of legislation for import enthusiasts. This federal law allows vehicles that are at least 25 years old to be imported into the U.S. without having to meet modern safety and emissions standards.

Why Age Matters for Insurance

From an insurance perspective, reaching that 25-year mark changes the vehicle's status from a "non-conforming liability" to a "classic or collector vehicle."

Safety Exemptions: Once a car hits 25, it is exempt from NHTSA crash-test requirements.

Emissions Exemptions: It is similarly exempt from EPA requirements in most cases.

Valuation Shift: At 25 years old, the vehicle is no longer seen as a "used car" but as a "collector asset."

If you are looking to insure a vehicle younger than 25 years, the process becomes exponentially more difficult and expensive, often requiring substantial modifications to meet U.S. standards. For most CT collectors, staying within the 25-year exemption window is the most viable path to securing gray market car insurance CT.

Key Challenges in Insuring Gray Market Classics

Insuring a rare import involves overcoming several hurdles that don't exist with a domestic Ford or Chevrolet. You are dealing with a vehicle that lacks a traditional U.S. history, making the underwriting process much more manual and intensive.

The 11-Digit VIN Hurdle

Most vehicles manufactured for the U.S. market after 1981 use a standardized 17-digit VIN. Imports, particularly those from Japan (JDM), often use much shorter chassis codes (e.g., BNR32-XXXXXX). Standard insurance software is hardwired to reject anything that isn't 17 digits. To insure these, your agent must manually override the system or work with a carrier like Hagerty or Grundy that understands how to process international chassis codes.

Determining "Agreed Value"

Traditional auto insurance uses "Actual Cash Value" (ACV), which factors in depreciation. If you insure a rare R32 Skyline under an ACV policy and it is totaled, the insurance company might try to value it as a "1990 Nissan Coupe," offering you a few thousand dollars for a car worth $60,000.

For rare imports, you must secure an Agreed Value policy. This is a contract where you and the insurer agree on the vehicle's value upfront. If a total loss occurs, that is the exact amount you are paid, minus your deductible. This protects your investment against the volatility of the import market.

Parts Availability and Repair Costs

Insurers are often wary of rare imports because of the "cost to repair." If your 1992 Autozam AZ-1 (a tiny Japanese gull-wing car) gets into a fender bender in Rocky Hill, the parts aren't sitting in a warehouse in Memphis. They likely have to be sourced from a specialty dismantler in Japan and shipped via air freight. Underwriters factor this potential "loss of use" and high parts cost into your premium.

Best Practices for Securing Rare Import Insurance in CT

Navigating the world of gray market insurance requires a proactive approach. You cannot simply call a 1-800 number and expect a favorable result. You need to treat the insurance application as a professional presentation of your vehicle’s worth and safety.

1. Document Everything

When you import a vehicle, you receive a mountain of paperwork. Keep every piece of it. To secure the best coverage, you will need to provide:

The HS-7 Form: Proof of legal entry through Customs.

The 3461 Entry Summary: Documentation of the duties paid.

The Export Certificate: The original title from the country of origin (and its certified translation).

High-Resolution Photos: Documentation of the car’s condition, including the engine bay, interior, and underside.

2. Establish a Realistic Valuation

Don't guess what your car is worth. Look at recent auction results from sites like Bring a Trailer or Cars & Bids. If you have spent $15,000 on a period-correct HKS turbo kit and Ohlins suspension, those receipts are vital. For high-value imports, getting a professional appraisal from a specialist who understands the JDM or EDM (European Domestic Market) is often the best way to justify your "Agreed Value" request.

3. Usage and Storage Requirements

Most specialized insurers will offer lower rates if you agree to certain conditions. These cars are meant for weekend drives through Litchfield County, not daily commutes to Hartford.

Garage Storage: Almost all rare import policies require the vehicle to be stored in a fully enclosed, locked garage.

Daily Driver Requirement: You will likely need to prove that every licensed member of your household has a separate "daily driver" vehicle insured elsewhere.

Mileage Limits: Many policies cap your annual mileage at 2,500 or 5,000 miles.

For more information on how different vehicle types are handled, you can explore our insurance blog articles which cover a wide range of specialty topics.

Why Connecticut Collectors Face Unique Situations

Connecticut has its own set of rules when it comes to registering and titling "Antique" vehicles. While the state is generally friendly to collectors, the DMV can be meticulous regarding VIN verification for out-of-country vehicles.

Because CT requires a VIN verification for any vehicle previously registered out of state or out of country, you will need to take your import to a designated inspection station. If the inspector cannot find a VIN that matches your paperwork, common in cars where the chassis code is stamped in a non-traditional location, you may face delays.

At Insure Connecticut LLC, we help our clients prepare for these hurdles by ensuring their insurance binders are perfectly aligned with their import documentation. If the DMV sees a discrepancy between your insurance card and your customs forms, they will not issue a plate. We make sure that doesn't happen.

If you are currently in the process of importing a vehicle and need to secure a binder for the DMV, you can request a quote form directly through our website to start the process.

Trends and the Future of the Gray Market

The landscape of rare imports is shifting rapidly. As more iconic 90s cars (the "Golden Era" of Japanese performance) become legal under the 25-year rule, the demand for specialized insurance is skyrocketing.

The Rise of Modern Classics

We are moving past the era where "collector cars" only meant 1960s Muscle Cars. Today, a 1999 Mitsubishi Lancer Evolution VI or a 1998 Subaru Impreza 22B is considered a blue-chip collectible. Insurance companies are having to adapt their underwriting models to account for these "modern classics" which feature advanced electronics and turbochargers that were unheard of in traditional vintage cars.

Electric Conversions

A new trend we are seeing in Connecticut is the importation of classic shells (like the original Mini Cooper or the Land Rover Series II) and converting them to electric power. This creates a unique insurance challenge: How do you value a 1970 car with a 2025 Tesla drivetrain? This requires a specialized "Modified Collector" policy that recognizes the value of the conversion while maintaining the classic status of the chassis.

FAQ: Common Concerns for Import Owners

Q: Can I insure my imported car as a regular daily driver? A: It is very difficult and usually not recommended. Standard carriers often lack the parts-sourcing networks for rare imports, and a daily driver policy uses Actual Cash Value, which will not protect your investment. You are much better off with a specialty policy.

Q: Does my homeowners insurance cover my car while it’s in the garage? A: No. Homeowners insurance specifically excludes motor vehicles. If your garage fires and your rare import is inside, you need a dedicated auto policy to cover the loss. For other home-related protections, you might consider dwelling fire insurance for the structure itself.

Q: What if I modified my import with aftermarket parts? A: You must disclose this. Many collector policies allow for "Agreed Value" that includes the cost of modifications. If you don't disclose them and have a claim, the insurer may only pay to return the car to stock condition: which might be impossible if the parts are rare.

Q: Is "Gray Market" the same as "Salvage Title"? A: Absolutely not. A gray market car can have a perfectly clean history; it simply wasn't built for the U.S. market. A salvage title means the car was previously declared a total loss. These are two very different categories in the eyes of an underwriter.

Q: Can I get insurance before the car arrives in the U.S.? A: You can secure "Marine Cargo Insurance" for the shipping process, but your Connecticut-based collector policy typically starts once the car clears customs and is on U.S. soil.

Conclusion: Protecting Your Passion

Owning a rare import or a gray market classic in Connecticut is a statement. It shows a dedication to automotive history and a desire for a unique driving experience. However, that uniqueness comes with a responsibility to protect your asset with the right coverage.

You wouldn't trust a general mechanic to rebuild a rare Italian V12; why would you trust a general insurance call center to protect your investment? The team at Insure Connecticut LLC lives and breathes the local car culture. We understand the nuances of the 25-year rule, the frustration of 11-digit VINs, and the absolute necessity of Agreed Value coverage.

Don't leave your "uninsurable" dream car to chance. Whether you are scouting a barn find in Burlington or awaiting a shipping container at the Port of New Haven, we are here to ensure that when your car finally hits the Connecticut roads, it is fully protected.

If you are ready to secure the specialized coverage your rare import deserves, or if you simply have questions about the process, contact us today. Let’s make sure your piece of automotive history is protected for the next 25 years and beyond.

Insure Connecticut, LLC 71 Raymond Road, West Hartford, CT 06107 Phone: 860-440-7324 Request a Quote Today

Comments