.png)

The Flow: Why Water Damage Liability is a Plumber's Best Friend

- W. Tom Polowy, MS

- 3 days ago

- 6 min read

The Midnight Fountain: Why Your Insurance Policy is More Important Than Your Pipe Wrench

Imagine this: It’s 2:00 AM on a Tuesday. You’re deep in sleep, dreaming about a world where every homeowner understands that "flushable" wipes are a lie. Suddenly, your phone buzzes. It’s a client from a job you finished yesterday afternoon. They aren’t calling to thank you for the sleek new vanity installation. They’re calling because their brand-new Brazilian cherry hardwood floors are currently serving as the bottom of a very expensive indoor swimming pool.

As a plumber in Connecticut, you don’t just deal with water; you deal with the potential energy of a homeowner’s worst nightmare. Whether you’re a solo operator in West Hartford or running a fleet of vans out of New Haven, the reality of the trade is that water always finds a way. And when it finds a way onto a $10,000 rug or into the electrical panel of a finished basement, the "flow" changes from a plumbing problem to a financial catastrophe.

This is where small business insurance ct stops being a line item on your expense sheet and starts being your best friend. At Insure Connecticut, LLC, we’ve seen how a single loose fitting can threaten a business’s entire future. We specialize in helping Connecticut contractors navigate the murky waters of liability insurance, ensuring that when the pipes burst, your bank account doesn't have to.

The High Cost of the "Hidden Leak": Benefits and Challenges of Liability Coverage

In the plumbing world, the biggest risks aren't always the ones you can see. Sure, a blowout during a pressure test is dramatic, but it’s the slow, silent drip behind a newly tiled wall that truly keeps tradespeople up at night. Water damage is unique because it is progressive. It doesn't just wet a surface; it warps wood, breeds mold, and compromises structural integrity.

The Financial Shield

The primary benefit of a robust commercial insurance policy is, quite simply, survival. For most small business owners in CT, a $50,000 property damage claim isn't something you can just "work off" over the next few weekends. It’s a business-ending event. General liability insurance covers the cost of repairs, the replacement of damaged property, and, perhaps most importantly, the legal fees if the client decides to take you to court.

The Professional Edge

There’s a misconception among some newer contractors that insurance is just a "tax" on doing business. In reality, it’s a marketing tool. High-end residential clients and commercial property managers in Connecticut won't even let you through the door without a Certificate of Insurance (COI). Having the right coverage shows you aren't just a guy with a torch and some solder; you’re a professional who takes responsibility for his work.

Visual: A gritty, close-up shot of a plumber’s hands tightening a heavy-duty pipe, highlighting the precision and risk involved in the trade.

The "Care, Custody, and Control" Challenge

One of the biggest hurdles plumbers face is understanding the exclusions in their policies. A common point of confusion is the "Care, Custody, and Control" exclusion. Standard liability usually covers the damage caused by your work (like the flooded basement), but it might not cover the cost of the specific pipe or fixture you were working on if you broke it. Navigating these nuances is why working with a local expert at Insure Connecticut, LLC is vital. We help you understand exactly where your protection starts and stops.

Best Practices: How to Keep Your Business High and Dry

Choosing the right small business insurance ct is only half the battle. To truly protect your reputation and your wallet, you need to combine your coverage with on-site best practices. Here is a checklist to ensure you’re operating at peak safety:

Document Everything: Before you turn a single valve, take photos of the existing conditions. If there was already mold or water damage, you need proof so you aren't blamed for it later.

The "Double Check" Protocol: Develop a standard operating procedure for every job. Pressure test every line, and then check it again ten minutes later. It sounds basic, but most insurance claims stem from simple human error.

Review Your Subcontractors: If you bring in a helper or another trade, ensure they have their own insurance. If they don't, any damage they cause could fall back on your policy, potentially spiking your premiums or exceeding your limits.

Verify Your Limits: A standard $1 million policy might seem like a lot until you’re working in a $4 million home in Greenwich. Ensure your limits reflect the value of the properties you’re working in.

Secure Your Gear: Plumbing isn't just about liability; it’s about your tools. Make sure your policy includes Inland Marine coverage (tool insurance) so that if your van is broken into, you aren't out of work for a week.

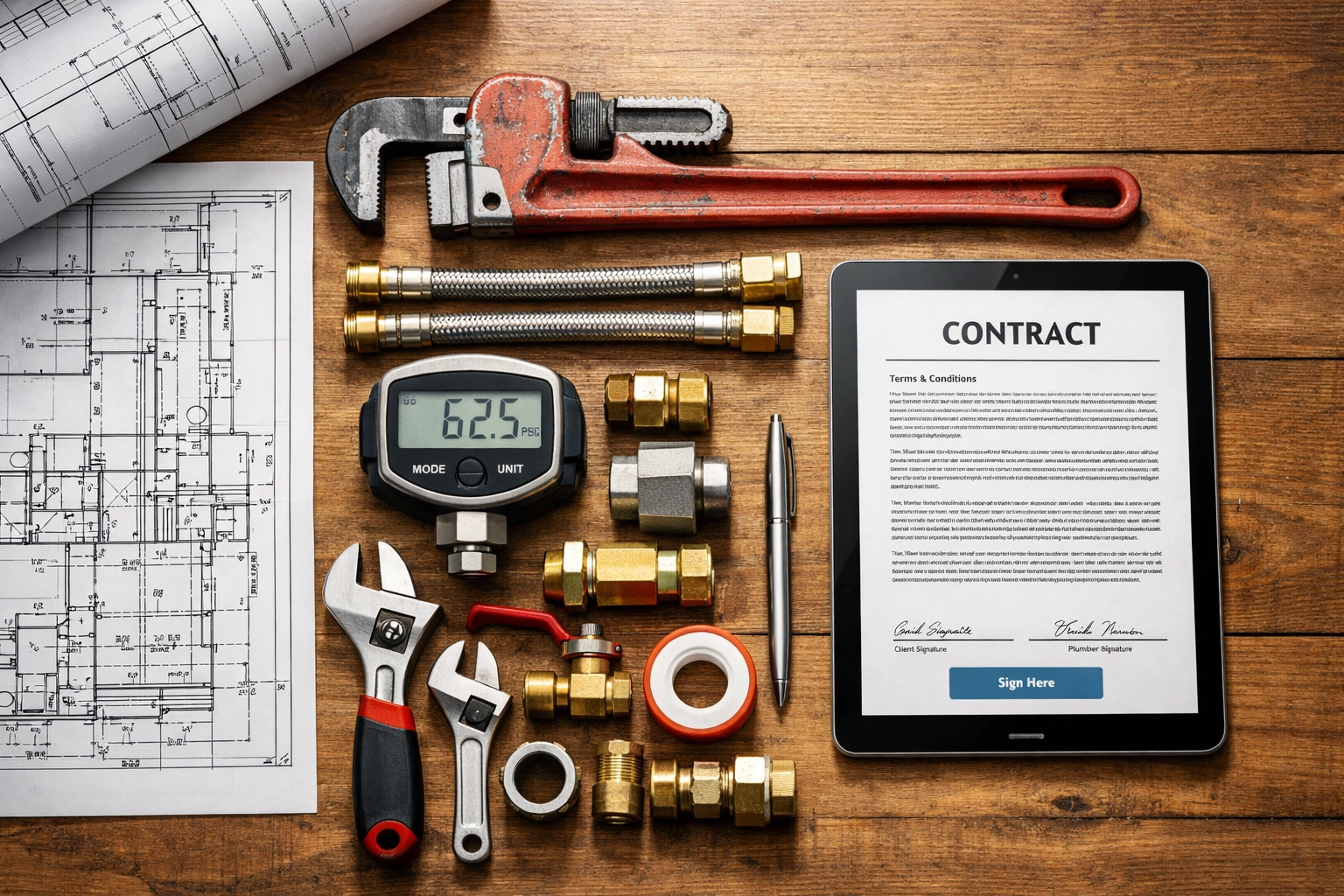

Visual: A clean, organized layout of plumbing tools, pipe cutters, wrenches, and gauges, on a blueprint, representing the intersection of manual skill and business planning.

Current Trends: The Future of Plumbing Risk in Connecticut

The plumbing industry isn't what it was thirty years ago. We are seeing a massive shift in both technology and regulation that affects your risk profile.

The Rise of Smart Home Technology

Many insurance companies are now offering discounts, or even requiring, the installation of smart leak detection systems. These devices can shut off the water main the moment they detect an unusual flow. As a plumber, being the person who recommends and installs these systems not only adds a revenue stream but also drastically reduces the likelihood of a massive liability claim.

Material Shifts and Longevity

The transition from copper to PEX has changed the "failure points" in modern plumbing. While PEX is easier to install, the risks associated with improper crimping or UV exposure create new types of liability. We stay on top of these trends at Insure Connecticut, LLC to ensure your property insurance and liability coverage keep pace with the materials you use every day.

Climate and Environmental Factors

Connecticut’s "freeze-thaw" cycles are getting more unpredictable. We are seeing an increase in claims related to burst pipes in poorly insulated areas. As a contractor, your advice on winterization is part of your professional service, and failing to warn a client about a vulnerable pipe could potentially lead to an errors and omissions claim.

FAQ: What Every CT Plumber Asks About Insurance

Q: Do I really need insurance if I’m just doing small residential repairs? A: Absolutely. A small leak in a second-floor bathroom can cause $20,000 in damage to the kitchen ceiling below. The size of the job doesn't dictate the size of the potential damage.

Q: What’s the difference between General Liability and Professional Liability for plumbers? A: General Liability covers physical damage (the flood). Professional Liability (or E&O) covers your advice and specialized services. If you design a complex commercial drainage system that fails to meet code, that’s where Professional Liability kicks in.

Q: Can I bundle my van insurance with my business liability? A: Yes, and you usually should. Bundling often leads to significant savings. You can learn more about how we handle home and auto and commercial vehicle combinations to keep your overhead low.

Q: How can I reduce my premiums without losing coverage? A: The best way to reduce premiums is to prove you are a low-risk contractor. Maintaining a clean claims history, using high-quality materials, and having a documented safety program can all help.

Q: Does my insurance cover me if my tools are stolen from the job site? A: Standard General Liability does not cover your tools. You need an "Inland Marine" or "Tools and Equipment" floater added to your policy. It’s a small addition that pays for itself the first time a saw goes missing.

Visual: The Insure Connecticut LLC Logo: A blue silhouette of Connecticut with a location pin containing a star above the text 'INSURECT'.

Conclusion: Don't Let Your Hard Work Go Down the Drain

Running a plumbing business in Connecticut is hard enough without having to worry if a single loose nut will bankrupt you. You spend your days ensuring "the flow" goes where it’s supposed to; let us do the same for your business protection.

At Insure Connecticut, LLC, we aren't just selling policies; we're building partnerships with the tradespeople who keep our state running. Whether you need to review your current small business insurance ct or you’re just starting out and need to know the basics of worker's compensation, we are here to help.

Ready to protect your business? Don't wait for the next leak to find out if you're covered.

Contact Insure Connecticut, LLC today: 📍 71 Raymond Road, West Hartford, CT 06107 📞 860-440-7324 🌐 www.myinsurect.com

Let’s make sure your insurance is as solid as your pipework. Give us a call, and let’s talk shop.

Comments