.png)

The Paperwork Trail: Certificates of Insurance (COI) 101

- W. Tom Polowy, MS

- 4 days ago

- 6 min read

Imagine this: You’ve spent weeks bidding on a high-stakes commercial renovation in downtown Hartford. You nailed the presentation, your numbers are tighter than a new pair of work boots, and you’re ready to break ground. You roll up to the job site, coffee in hand, only to be stopped at the gate by a site supervisor with a clipboard and a scowl.

"Where’s your COI?" he asks.

You reach into your glove box and pull out a 60-page stapled stack of paper, your entire insurance policy. The supervisor sighs. He doesn't want your life story; he wants your Golden Ticket. In the world of Connecticut business insurance, that ticket is the Certificate of Insurance.

At Insure Connecticut LLC, we see this play out every week. Business owners are experts at their craft, whether that’s plumbing, electrical work, or tech consulting, but the "paperwork trail" can feel like trekking through a swamp. Let’s clear the air and break down exactly what a COI is, why you need it yesterday, and how it keeps your business moving forward.

What is a Certificate of Insurance (COI), Anyway?

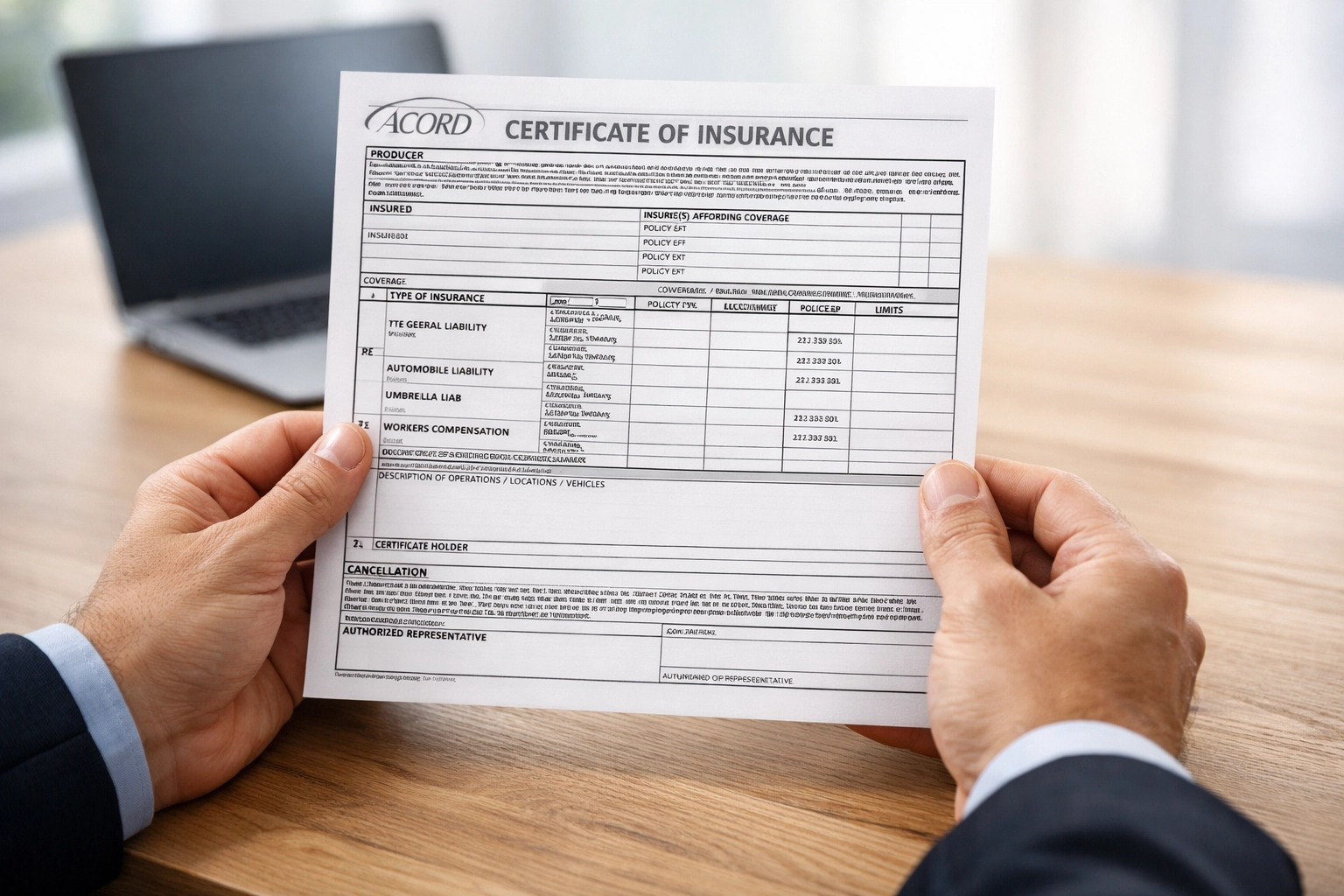

If an insurance policy is a 400-page novel, a COI is the "CliffsNotes" version. It is a standardized, one-page document (usually an ACORD 25 form) that summarizes the most important parts of your insurance coverage. It acts as official proof that you actually have the insurance you say you have.

Think of it like your driver’s license. When a police officer pulls you over, they don't want to see your birth certificate, your high school diploma, and your vehicle’s original manufacturing blueprint. They want that one little card that proves you are authorized to be behind the wheel. A COI does the same for your business liability.

The Anatomy of a COI: What’s Inside?

A standard COI isn't just a random list of numbers. It’s a strategic snapshot of your financial safety net. Here is what any savvy contractor or business owner should see when they look at one:

The Producer: This is us, Insure Connecticut LLC. It lists the agency that issued the certificate.

The Insured: That’s you and your business. Make sure the name matches your legal business entity exactly.

The Insurers: These are the actual insurance companies (carriers) providing the coverage.

Coverages: This section lists the types of insurance you have, General Liability, Commercial Auto, Workers’ Comp, and Umbrella policies.

Policy Limits: This shows the "how much." Usually, you’ll see numbers like $1,000,000 per occurrence and $2,000,000 aggregate.

Effective & Expiration Dates: This is the most common reason COIs get rejected. If your policy expired yesterday, that paper is just a fancy napkin.

Certificate Holder: This is the person or company who requested the proof (your client, the landlord, or the general contractor).

Why a COI is Your Best Sales Tool

Many business owners view the COI as a hurdle, a piece of red tape standing between them and a paycheck. But if you flip the script, a COI is actually one of the strongest marketing tools in your arsenal.

When you provide a clean, professional COI quickly, you are telling your client three things:

I am professional. You have your act together and understand the legal requirements of your industry.

I am solvent. You have the financial backing to handle a mistake if one happens.

I am low risk. You aren't a "tailgate contractor" working under the table; you are a legitimate entity protected by Connecticut business insurance.

In a competitive market like West Hartford or New Haven, being the guy who has his COI ready to go can be the tie-breaker that wins you the contract over the guy who says, "Uh, let me call my brother-in-law and see if I'm covered."

The "Additional Insured" Headache

If you’ve spent five minutes in the construction or service industry, you’ve heard the phrase "Additional Insured." This is usually where the confusion starts.

When a client asks to be named as an "Additional Insured," they aren't just asking for proof of your insurance. They are asking to be pulled under your umbrella. If something goes wrong on the job site and they get sued because of your work, your insurance policy will defend them too.

It sounds scary, but it’s a standard cost of doing business in CT. However, not all policies are created equal. Some "budget" policies don't allow for easy "Additional Insured" endorsements, which can lead to delays. This is why it's vital to work with an agency that understands the nuances of commercial auto insurance and general liability requirements.

Common COI Pitfalls (And How to Avoid Them)

We’ve seen it all at InsureCT. To keep your projects on track, watch out for these common "paperwork traps":

1. The Name Game

Does your COI say "John’s Plumbing" while your contract says "John Smith Plumbing, LLC"? If the names don't match exactly, the legal department at the big firm you’re working for will likely reject it. Precision matters.

2. Missing Workers’ Comp

In Connecticut, if you have even one employee, you need Workers’ Comp. If your COI shows General Liability but the Workers' Comp box is blank, many GCs won't let you set foot on the site. If you're a sole proprietor and exempt, you may need a specific waiver or a "ghost policy." We help clients navigate this daily to ensure they meet Workers' Comp requirements in CT.

3. Expired Dates

It sounds obvious, but you’d be surprised how many people try to use a COI from 2024 for a 2026 job. Set a calendar reminder 30 days before your policy renews so you can get your updated certificates out to your regular clients.

Best Practices for Managing Your Paperwork

If you want to spend more time working and less time wrestling with PDFs, follow this simple workflow:

Keep a Digital Folder: Save your most recent COI in a cloud folder (Google Drive, Dropbox) that you can access from your phone.

Ask for Requirements Early: Don't wait until the morning the job starts. Ask your client for their insurance requirements as soon as you start the bidding process.

Use an Agency That Moves Fast: At Insure Connecticut LLC, we know that in business, time is money. When you need a COI with a specific certificate holder listed, you shouldn't have to wait three days. We pride ourselves on getting these out the door so you can get to work.

Future Trends: The Digital COI

The days of faxing a grainy, crooked piece of paper are (thankfully) coming to an end. We are seeing a major shift toward digital verification. Many large Connecticut developers and property management firms now use third-party tracking software.

These platforms automatically "read" your COI and flag any deficiencies. This means your coverage needs to be "bulletproof." If your policy has a weird exclusion for "residential roofing" and you're trying to work on a condo complex, the software will catch it instantly. Staying ahead of these trends is part of our job at InsureCT: we make sure your Connecticut business insurance isn't just a piece of paper, but a functional part of your business growth.

Frequently Asked Questions (FAQ)

1. Does a COI mean I’m fully covered for everything?

No. A COI is just a summary. It doesn't list every exclusion or condition in your policy. For example, it might show you have Cyber Insurance, but it won't explain the specific cybersecurity requirements you must follow to maintain that coverage.

2. How much does it cost to get a COI?

Typically, your insurance agent should provide a standard COI for free. It's a service included in your policy management. However, if your client requires a "special endorsement" that isn't already in your policy, the insurance company might charge a small additional premium.

3. Can I just edit a COI myself in a PDF editor?

Absolutely not. Altering a COI is considered insurance fraud. It is a legal document issued by the agency or carrier. If you're caught "fixing" a date or a limit, you could lose your license, face massive fines, and be blacklisted from every job site in Connecticut.

4. What is a "Notice of Cancellation" on a COI?

This is a promise from the insurance company that if your policy gets cancelled (usually for non-payment), they will try to notify the certificate holder within a certain number of days (usually 30). It gives your clients peace of mind that you won't let your insurance lapse the moment you start the job.

5. Why do landlords always ask for a COI?

Landlords want to make sure that if you burn the building down or a customer slips in your shop, your insurance pays for the damage: not theirs. It's about shifting the risk to the party responsible for the daily operations.

Conclusion: Don't Let the Paperwork Trail Stop You

A Certificate of Insurance might look like just another boring form, but it is the backbone of business commerce in Connecticut. It builds trust, verifies protection, and opens doors that would otherwise remain locked.

Whether you are a startup in West Hartford or an established construction crew in Stamford, staying on top of your COI game is essential. Don't wait for a crisis or a rejected bid to realize your paperwork is out of order.

At Insure Connecticut LLC, we are more than just policy sellers: we are your back-office partners. We handle the paperwork trail so you can focus on building your legacy. If you need a review of your current Connecticut business insurance or need a COI issued for your next big project, give us a call at 860-440-7324 or stop by our office at 71 Raymond Road, West Hartford.

Let’s get your Golden Ticket ready for the next job site.

Comments